Nearly 30% of respondents said that retirement isn’t part of their current financial planning...

...and another 30% said pensions aren’t important to them.

Competing financial pressures mean people tend to focus on the present and seemingly more pressing financial matters like debt and financial dependants:

50% are paying off a loan or credit card, and 30% regularly use an overdraft (this is higher for those who are under 34 years old)

Many people’s budgets and spending are dominated by their dependants; 45% of people have financial dependants to support

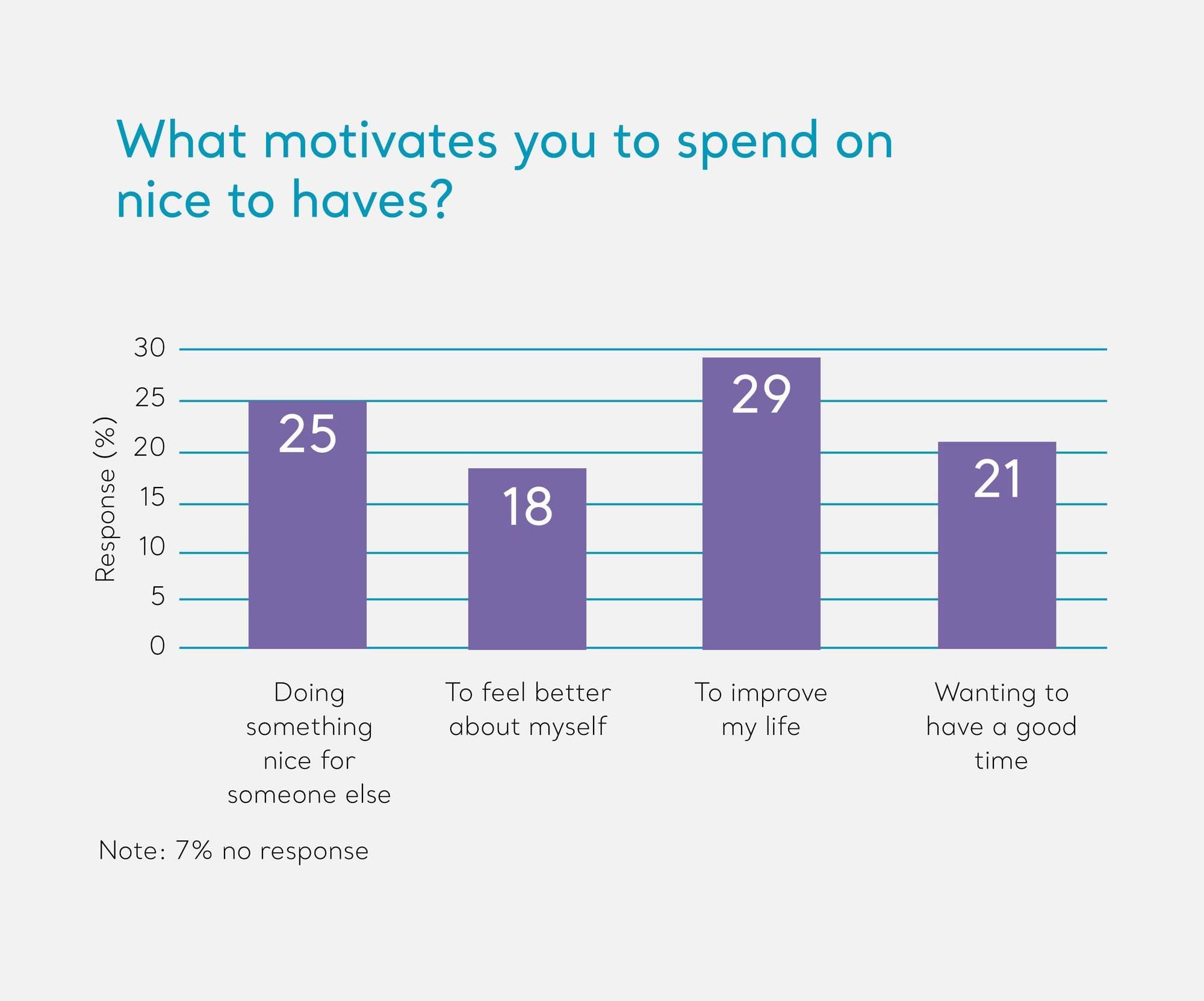

An ‘instant gratification’ pull is strong when it comes to spending and saving; people are more interested in having money/gratification now than in the future.

68% would prefer one luxury holiday now, than two luxury holidays later in retirement.

This theme represents two barriers that can obstruct changing pension behaviours for the better:

From a communications perspective, we can tackle these barriers head-on by driving pension awareness with a constant ‘savings drumbeat’ played throughout the organisation. Using affirmative messaging can also entice better savings behaviour.

Leading with what matters to employees now (their existing financial priorities), and tying pensions into this, is a subtle but effective pension engagement tactic. For example, workshops on budgeting or managing debt can introduce the positive benefits of auto enrolment, pensions and long-term savings.

By increasing the ‘pension beat’ within your organisation your business will inevitably benefit from greater pension engagement and as a result better appreciation and Return on Investment (ROI) on the pension benefit provided to employees. Enticing better pension behaviour will improve employees’ retirement readiness, and allow for better succession planning within your organisation.